VWAP for gold

Using 1h gold prices as input.

Loading data

from cipher import Cipher, Strategy

class VwapStrategy(Strategy):

pass

def main():

cipher = Cipher()

cipher.add_source(

"csv_file", path="data/gc1h.csv", ts_format="%d/%m/%YT%H:%M", delimiter=";"

)

cipher.set_strategy(VwapStrategy())

cipher.run(start_ts="2020-01-01", stop_ts="2020-02-01")

cipher.plot()

if __name__ == "__main__":

main()

Add VWAP

import talib

from cipher import Cipher, Session, Strategy

class VwapStrategy(Strategy):

def compose(self):

df = self.datas.df

df["price_volume"] = (df["high"] + df["low"]) / 2 * df["volume"]

daily = df.resample("24h").agg({"volume": "sum", "price_volume": "sum"})

daily = daily[daily["volume"] > 0]

df["vwap"] = (daily["price_volume"] / daily["volume"]).shift(1)

df["vwap"] = df["vwap"].fillna(method="ffill")

hlc3 = (df["close"] + df["high"] + df["low"]) / 3

df["ema"] = talib.EMA(hlc3, timeperiod=24)

df["long"] = (hlc3 > df["vwap"]) & (hlc3 > df["ema"])

df["short"] = (hlc3 < df["vwap"]) & (hlc3 < df["ema"])

return df

def on_long(self, row: dict, session: Session):

pass

def on_short(self, row: dict, session: Session):

pass

def main():

cipher = Cipher()

cipher.add_source(

"csv_file", path="data/gc1h.csv", ts_format="%d/%m/%YT%H:%M", delimiter=";"

)

cipher.set_strategy(VwapStrategy())

cipher.run(start_ts="2020-01-01", stop_ts="2020-02-28")

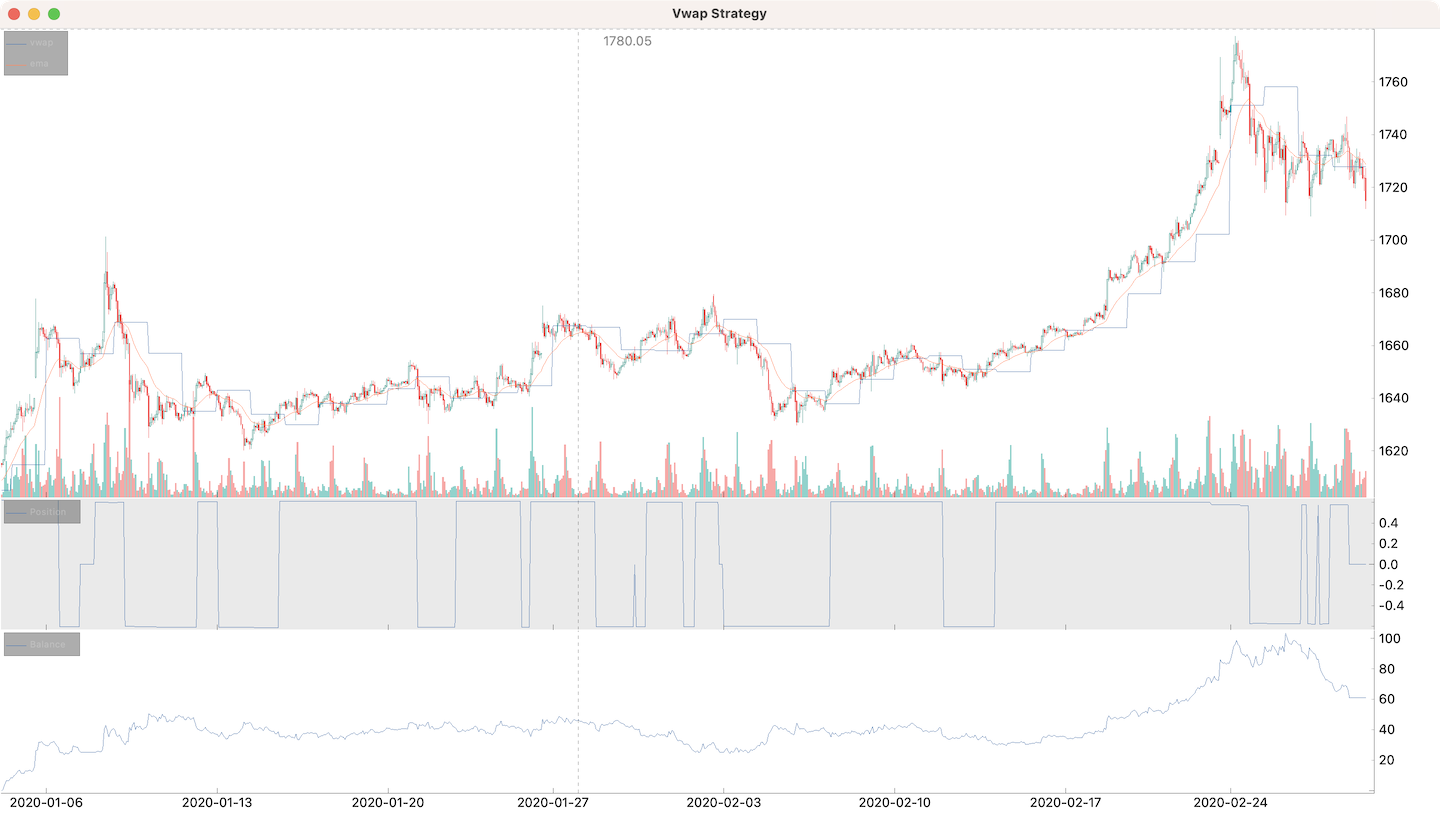

cipher.plot(rows=[["ohlcv", "vwap", "ema"], ["signals"]])

if __name__ == "__main__":

main()

Position

Take profit and stop loss 0.5% both. Trailing take profit.

import talib

from cipher import Cipher, percent, Session, Strategy, quote

class VwapStrategy(Strategy):

def compose(self):

df = self.datas.df

df["price_volume"] = (df["high"] + df["low"]) / 2 * df["volume"]

daily = df.resample("24h").agg({"volume": "sum", "price_volume": "sum"})

daily = daily[daily["volume"] > 0]

df["vwap"] = (daily["price_volume"] / daily["volume"]).shift(1)

df["vwap"] = df["vwap"].fillna(method="ffill")

hlc3 = (df["close"] + df["high"] + df["low"]) / 3

df["ema"] = talib.EMA(hlc3, timeperiod=24)

df["long"] = (hlc3 > df["vwap"]) & (hlc3 > df["ema"])

df["short"] = (hlc3 < df["vwap"]) & (hlc3 < df["ema"])

df["entry"] = df["long"] | df["short"]

return df

def on_entry(self, row: dict, session: Session):

if self.wallet.base != 0:

return

if row["long"]:

session.position += quote(1000)

session.take_profit = percent("0.5")

session.stop_loss = percent("-0.5")

else:

session.position -= quote(1000)

session.take_profit = percent("-0.5")

session.stop_loss = percent("0.5")

def on_take_profit(self, row: dict, session: Session):

if session.is_long:

session.take_profit = percent("0.5")

session.stop_loss = percent("-0.5")

else:

session.take_profit = percent("-0.5")

session.stop_loss = percent("0.5")

def main():

cipher = Cipher()

cipher.add_source(

"csv_file", path="data/gc1h.csv", ts_format="%d/%m/%YT%H:%M", delimiter=";"

)

cipher.set_strategy(VwapStrategy())

cipher.run(start_ts="2020-01-01", stop_ts="2020-02-28")

cipher.plot(rows=[["ohlcv", "vwap", "ema"], ["position"], ["balance"]])

if __name__ == "__main__":

main()

---------------- ---------------------- -----

start 2020-01-02 17:00

stop 2022-11-21 22:00

period 1054d 5h

trades 1237

longs 576 46.6%

shorts 661 53.4%

period median 10h

period max 8d 11h

success 484 39.1%

success median 4.97487500000000001

success max 61.6512699192029563

success row 6

failure 753 60.9%

failure median 5.0000000000000000

failure max 5.00000000000000001

failure row 11

spf 0.6427622841965471

pnl 216.01161017633149651

volume 1350.7660692182473918

commission 0

exposed period 1005d 23h 29m 11s 95.0%

balance min -0.0018596039285512234

balance max 378.80060115210904

balance drawdown 240.39084147373262

romad 0.8985850245045004

---------------- ---------------------- -----